There is a lot being spoken about the vote for the UK to leave the EU but I think it is time for everyone to slow down a bit and take the time to digest what has happened and think about the opportunity. Once when I was young and involved in national agri-politics here in Australia I tried to get four national bodies amalgamated into one (of course orders of magnitude less complex than the UK/EU situation). I lost that vote 17-16 on the conference floor. A wise old hand came up to me later and said “son, that is the best loss you will ever have”. What he meant was that a close yes vote would have emboldened the opponents to undermine any moves to make the vote into reality and caused more problems than it was worth.

The effort was subsequently re-attempted (not by me but with my support) and passed unanimously. I was asked to come back and chair the new body which has operated successfully ever since. Now the situation in the UK is much more complex but the principles are the same. The vote has a majority and that is how democracy works. However the margin is not large, and while governments have to be elected by a simple majority, making seismic decisions of the type that we are discussing here needs much more support by the people. From a distance the referendum seems to have riven the country more than just a simple 52-48 vote. The leave vote has a clear majority and is entitled to take that in the way that the referendum was intended. However there is a very large minority that disagreed. Within that difference there are significant fault lines:

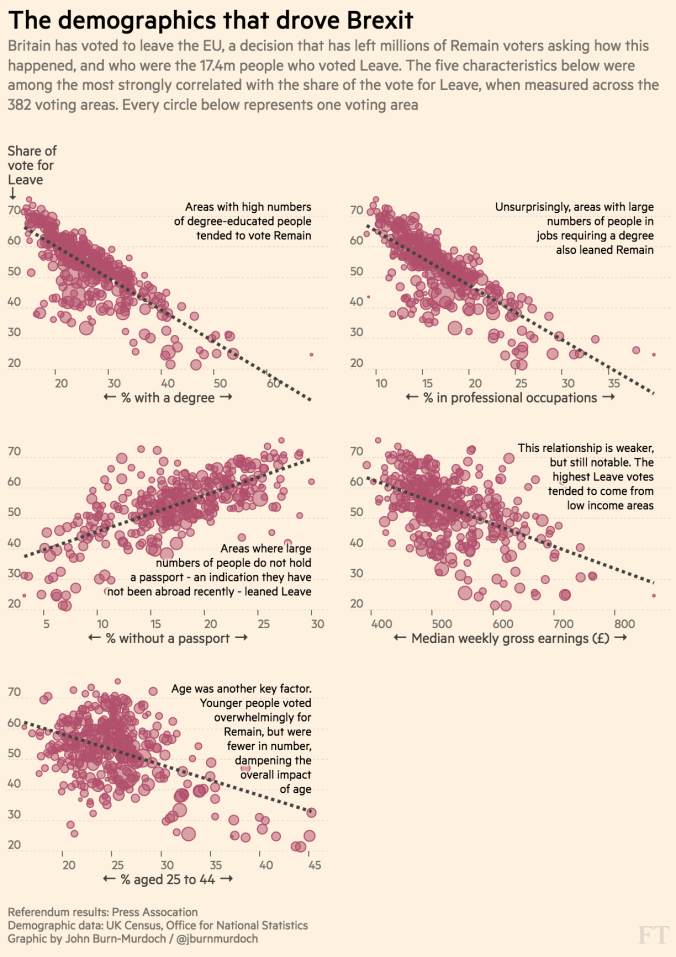

- The older people seem to have voted largely to leave while a large majority of those under 24 and under voted to stay.

- The Scots voted overwhelmingly to stay.

- Areas with people with a larger percentage of tertiary degrees voted to stay.

Source: http://blogs.ft.com/ftdata/2016/06/24/brexit-demographic-divide-eu-referendum-results/

There are other differences as well.

Again from a distance, the leave vote seems to be the combination of a number of sub groups with different concerns including the lack of real democracy in the EU, the effects of globalisation on their communities, the feeling that the political elites have ignored their concerns, issues with immigration, etc. I cannot possibly analyse these in any detail from a distance but I think the real opportunity is to really understand what has happened here and change political party attitudes and policies both in the EU and the UK. What has happened in the UK seems to be a microcosm of significant political disillusionment playing out across the world so we need to take the time to slow down and utilise the opportunity. This will take real leadership at every level and across the political divide, perhaps too much to expect?

In practical terms I think that this means:

Delaying any decision formally enact article 50 to start the negotiations to leave the EU. This is an enormously difficult and long process so the delay of a few months will not affect it adversely. This will give everyone a chance to sit back and think more deeply about what has happened and have calm negotiations.

Then the course can be:

1/ Enact article 50 and go through the process.

OR

2/ Revisit the referendum for a second vote.

Of course re-visiting the vote is fraught with problems. The leave vote can claim they have a clear mandate and it would be a disaster to run a second referendum and have the stay vote win 52-48. That would leave the country riven with deeper entrenched fault lines. Therefore it could only be done if:

1/ There is a genuine attempt by the major political parties to understand the political problems that have created the divide and address them via both domestic and European policy and legislation. This would have to include negotiation with the EU which they may or not wish to do (see EU leaders call for UK to leave as soon as possible ). Another reason for everyone to take a step back and think through things. It may be that negotiations with the UK could be helpful in precluding other problems within the EU.

2/ After that,and only after that there is a clear indication via respected and independent polling that a significant majority (say 60% or better) that they want a second referendum.

For this to be successful the subsequent vote would have to have a much clearer majority.

Personally I favour looking to see if the second referendum can work but the main thrust of what I am saying is that a calm and detailed analysis of what has happened should be the prelude to what happens next. Otherwise the UK risks being affected by the significant fault lines that underlie the votes of various groups. That could cause significantly more problems than staying in or leaving the EU.

As the cliche goes we should never miss the opportunity of a crisis.

Paul Higgins

Note: Before people start commenting about someone from the other side of the world commenting on this I was born in the North of the UK (Oldham, just near Manchester) and still hold dual passports. I still have lots of family there and have visited several time and just this month had family here from the UK discussing the referendum at length. I also have some experience in politics having been President of Country Labor in Victoria here and running for Federal pre-selection twice in regional seats. So I have some experience in the difference between city and regional people and their politics, albeit in a different country. Having said that it should be the thinking that is critiqued.