In conjunction with the announcement by Tesla on April 30th that they are supplying home battery storage systems (Tesla launches a stationary battery aimed at companies with variable electricity rates and homes with solar panels.) Solar City in the USA has announced that

Just think about that for a moment. A model which has dropped in price by 67% in 12 months. That is disruption on a major scale.

The solar panel business and the battery storage business is likely to be a continually brutal Darwinian space and require huge capital to supply the necessary scale because of the structure of the technology and the cost reductions that are occurring.

This raises the question of what is the smart play in this space and I think it is in staying away from the panel and battery technology space and playing in business model innovation at the layer above that.

There has been considerable comment on what is happening in the cost curve reductions in solar panels and battery storage including:

Why Moore’s Law Doesn’t Apply to Clean Technologies

and a counterpoint from one of my favourite analysts/writers Ramez Naam:

Is Moore’s Law Really a Fair Comparison for Solar?

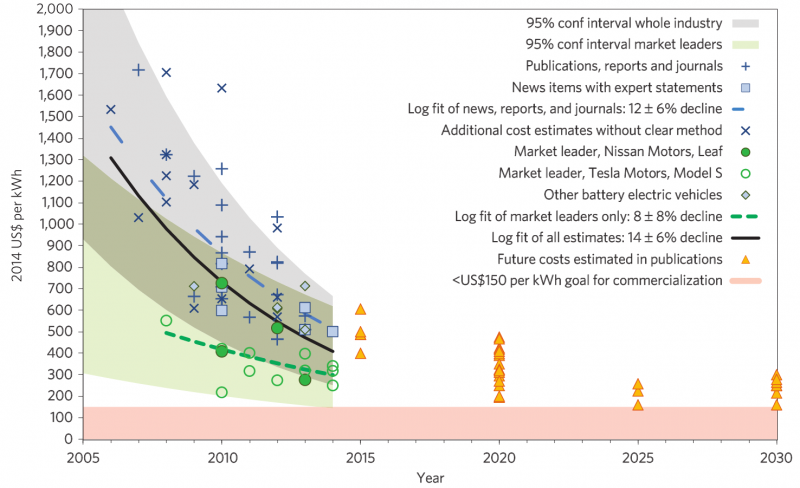

who embedded the following graphic from Nature Climate Change

looking at the falling prices in battery storage.

I think both articles make excellent points but the main issue is the cause of price change over time which has been 60% annually for transistors and 14% annually for solar (over 37 years) according to Naam. Analysis of the two articles indicates that the change in transistors has been far more driven by technological innovation while the pace in solar has been more by the classic cost learning curve and move to scale.

Which brings us to the smart play. My view on the key drivers when thinking about business strategy:

- Just as many solar manufacturers have bitten the dust over the last decade the same will apply to battery manufacturers and start up battery companies in the next decade, as well as being a continuing issue in the panel industry.

- One of the main problems with Lithium Ion batteries is the charge and discharge cycle lifetime. From a cost per kWh storage point of view the shorter the life cycle then the higher the cost as the initial capital costs have to be depreciated over less energy usage. Therefore alternative battery storage options have to be a key competitor in the space. There is lots of investment going on in technology development. So to win you either have to have the capital backing that companies like Tesla boast or pick the right technology and take the development risk.

- Particularly at a household level the costs are related as much to installation and deployment model as to cost of the technology (just as transistors are only a fraction of smartphone or tablet costs).

- At the household level adoption issues beyond costs will also be critical.

So while there will be clearly winners in the panel and battery space the risks and capital required are enormous. There are better opportunities in deploying innovative business models in the space including:

- Models for landlords that get around the issues of the landlords bearing the capital costs and tenants gaining the cost reduction on their power bills. This includes leasing and income sharing models driven by algorithms.

- Efficient and low cost installation models that drive down the costs of installation and maintenance.

- Financing models that allow installation for people that otherwise could not afford installation.

- Community models that integrate use of the grid into distributed generation, storage and consumption models that reduce costs to consumers while improving the income for local generators and renewable energy systems

There are parallels for this in other sectors. The sports clothing company Under Armour is pursuing a strategy for fitness apps to complement its sports clothing sales. That strategy is hardware technology agnostic in that it integrates with a range of technologies that users are adopting. This means they do not tie themselves to any particular hardware solution and avoid riding on top of a technology that fails.

That is the smart play here

Paul Higgins

Full disclosure: I have recently worked for the sugar milling industry here in Australia on energy transition scenarios. I may in the future have a financial interest in community models.